Global steel market to reach USD 1,308.7B by 2034, driven by aerospace, shipbuilding, appliances, and rising manufacturing demand.

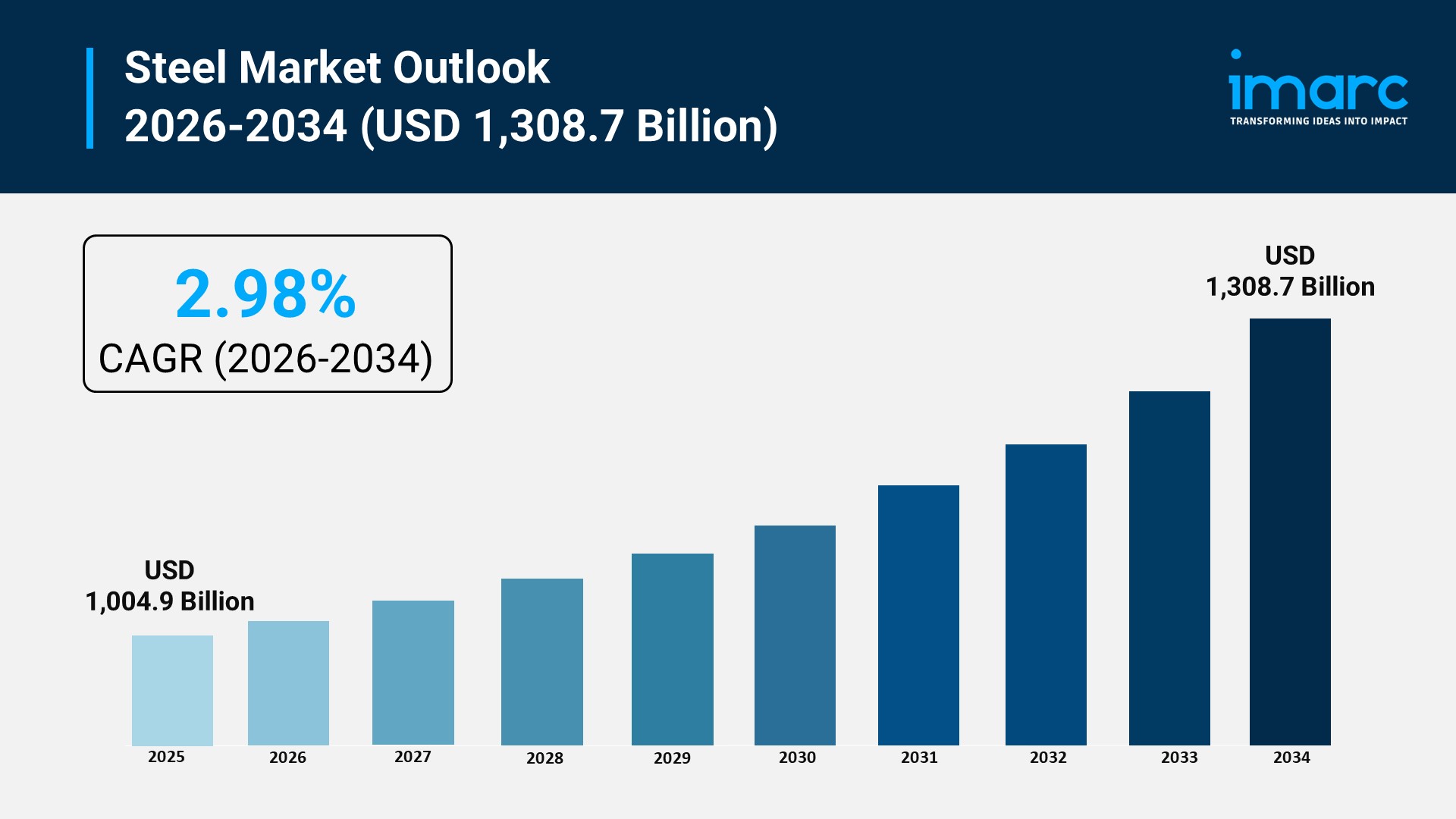

SHERDIAN, WY, UNITED STATES, May 13, 2026 /EINPresswire.com/ — The global steel market was valued at 𝐔𝐒𝐃 𝟏,𝟎𝟎𝟒.𝟗 𝐁𝐢𝐥𝐥𝐢𝐨𝐧 in 2025 and is projected to reach 𝐔𝐒𝐃 𝟏,𝟑𝟎𝟖.𝟕 𝐁𝐢𝐥𝐥𝐢𝐨𝐧 by 2034, expanding at a 𝐂𝐀𝐆𝐑 𝐨𝐟 𝟐.𝟗𝟖% during 2026–2034, according to the latest market research report by IMARC Group. Growth is driven by Asia Pacific’s dominant regional share of over 62.7%, the leading role of Building and Construction applications (49.0% share), Long Steel as the top product type (49.0%), and accelerating demand from automotive, military, and renewable energy sectors.

𝐑𝐞𝐩𝐨𝐫𝐭 𝐇𝐢𝐠𝐡𝐥𝐢𝐠𝐡𝐭𝐬

𝐌𝐚𝐫𝐤𝐞𝐭 𝐒𝐢𝐳𝐞 (𝟐𝟎𝟐𝟓): 𝐔𝐒𝐃 𝟏,𝟎𝟎𝟒.𝟗 𝐁𝐢𝐥𝐥𝐢𝐨𝐧

𝐅𝐨𝐫𝐞𝐜𝐚𝐬𝐭 (𝟐𝟎𝟑𝟒): 𝐔𝐒𝐃 𝟏,𝟑𝟎𝟖.𝟕 𝐁𝐢𝐥𝐥𝐢𝐨𝐧

𝐂𝐀𝐆𝐑 (𝟐𝟎𝟐𝟔–𝟐𝟎𝟑𝟒): 𝟐.𝟗𝟖%

𝐋𝐞𝐚𝐝𝐢𝐧𝐠 𝐑𝐞𝐠𝐢𝐨𝐧: 𝐀𝐬𝐢𝐚 𝐏𝐚𝐜𝐢𝐟𝐢𝐜 (𝟔𝟐.𝟕%+)

𝐓𝐨𝐩 𝐀𝐩𝐩𝐥𝐢𝐜𝐚𝐭𝐢𝐨𝐧: 𝐁𝐮𝐢𝐥𝐝𝐢𝐧𝐠 𝐚𝐧𝐝 𝐂𝐨𝐧𝐬𝐭𝐫𝐮𝐜𝐭𝐢𝐨𝐧 (𝟒𝟗.𝟎%)

𝐋𝐞𝐚𝐝𝐢𝐧𝐠 𝐓𝐲𝐩𝐞: 𝐋𝐨𝐧𝐠 𝐒𝐭𝐞𝐞𝐥 (𝟒𝟗.𝟎% 𝐬𝐡𝐚𝐫𝐞)

𝐓𝐨𝐩 𝐏𝐫𝐨𝐝𝐮𝐜𝐭: 𝐒𝐭𝐫𝐮𝐜𝐭𝐮𝐫𝐚𝐥 𝐒𝐭𝐞𝐞𝐥 (𝟒𝟓.𝟓% 𝐬𝐡𝐚𝐫𝐞)

𝐃𝐨𝐰𝐧𝐥𝐨𝐚𝐝 𝐚 𝐅𝐫𝐞𝐞 𝐒𝐚𝐦𝐩𝐥𝐞 𝐂𝐨𝐩𝐲 𝐨𝐟 𝐭𝐡𝐞 𝐑𝐞𝐩𝐨𝐫𝐭: https://www.imarcgroup.com/steel-market/requestsample

𝐒𝐭𝐞𝐞𝐥 𝐌𝐚𝐫𝐤𝐞𝐭 𝐎𝐮𝐭𝐥𝐨𝐨𝐤 𝟐𝟎𝟐𝟔–𝟐𝟎𝟑𝟒

Steel is a fundamental material underpinning modern civilization, serving as the backbone of construction, automotive manufacturing, energy infrastructure, military applications, and consumer goods. Its unparalleled strength, versatility, and recyclability position it as an irreplaceable input across virtually every major industry worldwide.

The market was valued at USD 1,004.9 Billion in 2025 and is projected to reach USD 1,308.7 Billion by 2034 at a 2.98% CAGR, driven by expanding construction and infrastructure investment globally, growing automotive production including electric vehicles, escalating defense spending, and the accelerating transition to renewable energy which demands steel for wind turbines and solar panel structures.

𝐒𝐭𝐞𝐞𝐥 𝐌𝐚𝐫𝐤𝐞𝐭 𝐃𝐫𝐢𝐯𝐞𝐫𝐬 𝟐𝟎𝟐𝟔

𝐒𝐢𝐠𝐧𝐢𝐟𝐢𝐜𝐚𝐧𝐭 𝐆𝐫𝐨𝐰𝐭𝐡 𝐢𝐧 𝐭𝐡𝐞 𝐆𝐥𝐨𝐛𝐚𝐥 𝐀𝐮𝐭𝐨𝐦𝐨𝐭𝐢𝐯𝐞 𝐈𝐧𝐝𝐮𝐬𝐭𝐫𝐲

The expansion of the global automotive industry is a primary catalyst for steel demand, as the material is integral to vehicle structural integrity, safety systems, and lightweight efficiency components. Original equipment manufacturers (OEMs) have collectively committed over USD 500 Billion toward establishing electric vehicle (EV) production facilities by 2030, including Hyundai’s USD 1.5 Billion investment in a new EV factory in Ulsan, South Korea announced in November 2023. Automakers are increasingly deploying advanced high-strength and lightweight steel alloys to meet evolving emissions regulations and consumer expectations, driving sustained demand for innovative steel solutions across the automotive sector.

𝐑𝐢𝐬𝐢𝐧𝐠 𝐃𝐞𝐦𝐚𝐧𝐝 𝐟𝐨𝐫 𝐒𝐭𝐞𝐞𝐥 𝐢𝐧 𝐌𝐢𝐥𝐢𝐭𝐚𝐫𝐲 𝐀𝐢𝐫𝐜𝐫𝐚𝐟𝐭 𝐌𝐚𝐧𝐮𝐟𝐚𝐜𝐭𝐮𝐫𝐢𝐧𝐠

Escalating global defense spending is a key driver for steel consumption, particularly in the aerospace and defense sector. Military aircraft require materials offering exceptional tensile strength and durability, with steel serving as the preferred choice for airframes, landing gear, engine components, and structural elements in fighter jets, transport aircraft, and helicopters. World military spending increased 3.7% in 2022, with the five largest spenders the United States, China, Russia, India, and Saudi Arabia collectively accounting for 63% of global defense expenditure. The geopolitical environment, including the ongoing Russia-Ukraine conflict, has accelerated defense modernization programs worldwide, reinforcing sustained demand for high-performance steel in military applications.

𝐑𝐚𝐩𝐢𝐝 𝐓𝐞𝐜𝐡𝐧𝐨𝐥𝐨𝐠𝐢𝐜𝐚𝐥 𝐀𝐝𝐯𝐚𝐧𝐜𝐞𝐦𝐞𝐧𝐭𝐬 𝐚𝐧𝐝 𝐑𝐞𝐧𝐞𝐰𝐚𝐛𝐥𝐞 𝐄𝐧𝐞𝐫𝐠𝐲 𝐄𝐱𝐩𝐚𝐧𝐬𝐢𝐨𝐧

Rapid technological progress across manufacturing, energy, and transportation is generating new and expanding demand for steel. The global push toward renewable energy including solar farms and wind turbines depends critically on steel for structural components. In 2022, the International Energy Agency reported that 14% of all new cars sold were electric, with China accounting for approximately 60% of global EV sales. Europe recorded a 15%+ increase in EV sales in the same period, while the United States saw a 55% surge. The growing application of the Internet of Things (IoT), automation, and smart manufacturing further reinforces steel’s role as a critical material in building next-generation industrial infrastructure.

𝐒𝐩𝐞𝐚𝐤 𝐃𝐢𝐫𝐞𝐜𝐭𝐥𝐲 𝐰𝐢𝐭𝐡 𝐚𝐧 𝐀𝐧𝐚𝐥𝐲𝐬𝐭 𝐟𝐨𝐫 𝐂𝐮𝐬𝐭𝐨𝐦𝐢𝐳𝐞𝐝 𝐈𝐧𝐬𝐢𝐠𝐡𝐭𝐬: https://www.imarcgroup.com/request?type=report&id=5712&flag=C

𝐒𝐭𝐞𝐞𝐥 𝐌𝐚𝐫𝐤𝐞𝐭 𝐓𝐫𝐞𝐧𝐝𝐬 𝟐𝟎𝟐𝟔

• 𝐀𝐝𝐨𝐩𝐭𝐢𝐨𝐧 𝐨𝐟 𝐀𝐝𝐯𝐚𝐧𝐜𝐞𝐝 𝐏𝐚𝐜𝐤𝐚𝐠𝐢𝐧𝐠 𝐚𝐧𝐝 𝐒𝐮𝐬𝐭𝐚𝐢𝐧𝐚𝐛𝐥𝐞 𝐒𝐭𝐞𝐞𝐥 𝐏𝐫𝐚𝐜𝐭𝐢𝐜𝐞𝐬

The adoption of advanced packaging solutions in food and beverage storage is fueling steel demand, leveraging the material’s high durability and recyclability. Simultaneously, the steel industry is increasingly embracing green manufacturing practices to reduce environmental impact and align with international emissions targets. A landmark example is the October 2024 memorandum of understanding between India’s JSW Group and South Korea’s POSCO to build an integrated steel plant in India with 5 million tonnes of annual capacity using green technologies, signaling a major industry-wide shift toward sustainable production.

• 𝐄𝐱𝐩𝐚𝐧𝐬𝐢𝐨𝐧 𝐢𝐧 𝐂𝐨𝐧𝐬𝐭𝐫𝐮𝐜𝐭𝐢𝐨𝐧, 𝐈𝐧𝐟𝐫𝐚𝐬𝐭𝐫𝐮𝐜𝐭𝐮𝐫𝐞, 𝐚𝐧𝐝 𝐔𝐫𝐛𝐚𝐧 𝐃𝐞𝐯𝐞𝐥𝐨𝐩𝐦𝐞𝐧𝐭

Global urbanization and infrastructure investment are sustaining robust steel consumption. In the United States, construction spending grew 10.9% year-on-year in April 2024, with manufacturing construction surging 17.3%, driven by landmark federal programs including the CHIPS Act and the Inflation Reduction Act (IRA). Monthly manufacturing construction spending has more than doubled since the introduction of these programs, exceeding USD 200 Billion. In India, demand for steel is projected to reach between 240 and 260 million metric tons by 2035, representing a CAGR of approximately 6% from 2023, supported by the National Steel Policy targeting 300 million tons of domestic production by 2030.

• 𝐑𝐞𝐜𝐲𝐜𝐥𝐢𝐧𝐠, 𝐂𝐢𝐫𝐜𝐮𝐥𝐚𝐫 𝐄𝐜𝐨𝐧𝐨𝐦𝐲, 𝐚𝐧𝐝 𝐆𝐫𝐞𝐞𝐧 𝐒𝐭𝐞𝐞𝐥 𝐈𝐧𝐧𝐨𝐯𝐚𝐭𝐢𝐨𝐧

Innovations in recycling and circular economy practices are enhancing the cost effectiveness and environmental performance of the steel sector, reinforcing its long-term market outlook. In the Middle East and Africa, a rising focus on carbon-emission reduction is driving growing interest in low-carbon and renewable-fuel steelmaking. China’s national steel policy targets a 30% reduction in steel industry emissions by 2025 through modernization and technology adoption. These trends are fostering a more sustainable and globally competitive steel industry that aligns with international climate commitments.

• 𝐍𝐞𝐚𝐫𝐬𝐡𝐨𝐫𝐢𝐧𝐠 𝐚𝐧𝐝 𝐏𝐫𝐞𝐟𝐚𝐛𝐫𝐢𝐜𝐚𝐭𝐢𝐨𝐧 𝐃𝐫𝐢𝐯𝐢𝐧𝐠 𝐍𝐞𝐰 𝐃𝐞𝐦𝐚𝐧𝐝 𝐂𝐞𝐧𝐭𝐞𝐫𝐬

Nearshoring trends are creating new centers of steel demand, particularly in Mexico, which ranks 14th globally among steel producers and serves as the second-largest steel supplier to the United States. Growth in Mexico’s steel market is projected at 1.5% to 2%, supported by construction sector expansion and nearshoring-driven industrial activity. Additionally, the increasing adoption of prefabricated and modular construction methods is strengthening demand for structural steel components, as these techniques require precision-engineered steel products that accelerate build timelines and reduce on-site labor costs.

𝐒𝐭𝐞𝐞𝐥 𝐈𝐧𝐝𝐮𝐬𝐭𝐫𝐲 𝐒𝐞𝐠𝐦𝐞𝐧𝐭𝐚𝐭𝐢𝐨𝐧

𝐀𝐧𝐚𝐥𝐲𝐬𝐢𝐬 𝐛𝐲 𝐓𝐲𝐩𝐞 (𝟐𝟎𝟐𝟓 𝐒𝐡𝐚𝐫𝐞)

• Long Steel – 49.0% (Leading)

• Flat Steel

Long steel leads the market with a 49.0% share in 2025. Products such as rebars, wire rods, and structural sections dominate due to their essential role in construction and infrastructure projects. Rebars reinforce concrete in residential, commercial, and industrial constructions, while wire rods serve diverse manufacturing and automotive applications. The rising adoption of prefabricated building techniques further strengthens demand for structural long steel components, alongside growing preference for recyclable, high-strength materials aligned with sustainable construction practices.

𝐀𝐧𝐚𝐥𝐲𝐬𝐢𝐬 𝐛𝐲 𝐏𝐫𝐨𝐝𝐮𝐜𝐭 (𝟐𝟎𝟐𝟓 𝐒𝐡𝐚𝐫𝐞)

• Structural Steel – 45.5% (Leading)

• Prestressing Steel

• Bright Steel

• Welding Wire and Rod

• Iron Steel Wire

• Ropes

• Braids

Structural steel leads the product segment with a 45.5% share, underpinned by its durability, versatility, and cost efficiency in construction and infrastructure applications including skyscrapers, bridges, factories, and transport networks. Growing urban development, renewable energy structures such as solar farms and wind turbines, and the increasing adoption of modular construction methods sustain demand for structural steel. Its high recyclability also aligns with global sustainability objectives, further supporting its dominance across the product landscape.

𝐀𝐧𝐚𝐥𝐲𝐬𝐢𝐬 𝐛𝐲 𝐀𝐩𝐩𝐥𝐢𝐜𝐚𝐭𝐢𝐨𝐧 (𝟐𝟎𝟐𝟓 𝐒𝐡𝐚𝐫𝐞)

• Building and Construction – 49.0% (Leading)

• Electrical Appliances

• Metal Products

• Automotive

• Transportation

• Mechanical Equipment

• Domestic Appliances

Building and construction leads the application segment with a 49.0% share, as steel is indispensable for beams, columns, and reinforcing bars that ensure structural strength and integrity across residential, commercial, and infrastructure projects. Ongoing urbanization, population growth, and global infrastructure investment sustain robust demand in this segment. Electrical appliances represent another significant end-use category, with stainless steel favored for its corrosion resistance in refrigerators, washing machines, and ovens. Continuous consumer demand for household appliances, driven by lifestyle improvements and technological advancement, ensures steady steel component requirements.

𝐑𝐞𝐠𝐢𝐨𝐧𝐚𝐥 𝐈𝐧𝐬𝐢𝐠𝐡𝐭𝐬: 𝐒𝐭𝐞𝐞𝐥 𝐌𝐚𝐫𝐤𝐞𝐭

𝐀𝐬𝐢𝐚 𝐏𝐚𝐜𝐢𝐟𝐢𝐜 – 𝐌𝐚𝐫𝐤𝐞𝐭 𝐋𝐞𝐚𝐝𝐞𝐫 (𝟔𝟐.𝟕%+ 𝐒𝐡𝐚𝐫𝐞)

Asia Pacific commands the largest share of the global steel market at over 62.7% in 2025, driven by extensive infrastructure development, a robust automotive manufacturing sector, diverse industrial activity, and rapidly expanding consumer goods and renewable energy industries. India’s steel demand is projected to reach 240–260 million metric tons by 2035 at a CAGR of approximately 6% from 2023, supported by the National Steel Policy targeting 300 million tons of domestic production by 2030. China continues to pursue large-scale steel sector modernization, targeting a 30% reduction in emissions by 2025 while APAC governments introduce national steel policies focused on local production and reduced import dependency.

𝐍𝐨𝐫𝐭𝐡 𝐀𝐦𝐞𝐫𝐢𝐜𝐚 – 𝐔𝐧𝐢𝐭𝐞𝐝 𝐒𝐭𝐚𝐭𝐞𝐬 𝐋𝐞𝐚𝐝𝐬 𝐰𝐢𝐭𝐡 𝟖𝟗.𝟓𝟎% 𝐑𝐞𝐠𝐢𝐨𝐧𝐚𝐥 𝐒𝐡𝐚𝐫𝐞

The United States accounted for over 89.50% of the North American steel market in 2025, underpinned by expanding construction and real estate sectors, federal infrastructure modernization programs, and a revival in manufacturing activity. The CHIPS Act and the Inflation Reduction Act have been transformative drivers, propelling monthly manufacturing construction spending beyond USD 200 Billion more than double since their introduction and making manufacturing construction the largest category of non-residential construction in the country. Advanced automotive manufacturing, renewable energy infrastructure, and domestic trade policies protecting local production further support long-term market growth.

𝐄𝐮𝐫𝐨𝐩𝐞 – 𝐈𝐧𝐝𝐮𝐬𝐭𝐫𝐢𝐚𝐥 𝐏𝐨𝐰𝐞𝐫𝐡𝐨𝐮𝐬𝐞 𝐚𝐧𝐝 𝐒𝐮𝐬𝐭𝐚𝐢𝐧𝐚𝐛𝐢𝐥𝐢𝐭𝐲 𝐋𝐞𝐚𝐝𝐞𝐫

Europe’s steel sector contributes 1.3% to the EU’s GDP, directly employs 328,000 individuals, and supports over two million indirect jobs through the supply chain and related industries. The region is recognized for its modern, energy-efficient, and CO2-efficient steel plants producing high-value specialized products for global markets, supported by a robust research and development ecosystem. The steel sector is a cornerstone of European automotive, machinery, and industrial competitiveness, and continued investment in innovation and low-carbon steelmaking is critical to maintaining Europe’s industrial leadership on the world stage.

𝐋𝐚𝐭𝐢𝐧 𝐀𝐦𝐞𝐫𝐢𝐜𝐚 – 𝐒𝐭𝐫𝐚𝐭𝐞𝐠𝐢𝐜 𝐈𝐧𝐯𝐞𝐬𝐭𝐦𝐞𝐧𝐭 𝐚𝐧𝐝 𝐏𝐨𝐥𝐢𝐜𝐲-𝐃𝐫𝐢𝐯𝐞𝐧 𝐆𝐫𝐨𝐰𝐭𝐡

Brazil is at the forefront of Latin America’s steel growth, with investments totaling Brazilian Real 100 Billion (USD 16.5 Billion) directed toward expanding production capacity, modernizing existing facilities, and constructing new plants with state-of-the-art technologies. Government tax incentives, regulatory reforms, and infrastructure improvements underpin this investment, with major milestones expected by 2028. Mexico, the world’s 14th-largest steel producer and second-largest supplier to the United States, is experiencing growth of 1.5%–2%, driven by nearshoring trends and rising construction sector demand.

𝐌𝐢𝐝𝐝𝐥𝐞 𝐄𝐚𝐬𝐭 𝐚𝐧𝐝 𝐀𝐟𝐫𝐢𝐜𝐚 – 𝐆𝐫𝐞𝐞𝐧 𝐒𝐭𝐞𝐞𝐥 𝐚𝐧𝐝 𝐆𝐨𝐯𝐞𝐫𝐧𝐦𝐞𝐧𝐭-𝐃𝐫𝐢𝐯𝐞𝐧 𝐄𝐱𝐩𝐚𝐧𝐬𝐢𝐨𝐧

The Middle East and Africa steel market is growing through a combination of green manufacturing practices and strong government initiatives. Oman’s steel sector directly employs 1,681 workers at an Omanization rate of 45%, reflecting the sector’s importance to national economic development. The UAE’s ambitious “Projects of the 50” initiative is projected to attract approximately USD 150 Billion in foreign direct investment by 2030, driving significant expansion in construction, transportation, and energy infrastructure all of which are major steel consumers. The region is increasingly positioning itself as a global leader in low-carbon steelmaking, aligning with international sustainability commitments.

𝐕𝐢𝐞𝐰 𝐭𝐡𝐞 𝐅𝐮𝐥𝐥 𝐑𝐞𝐩𝐨𝐫𝐭: https://www.imarcgroup.com/steel-market

𝐊𝐞𝐲 𝐂𝐨𝐦𝐩𝐚𝐧𝐢𝐞𝐬 𝐢𝐧 𝐭𝐡𝐞 𝐒𝐭𝐞𝐞𝐥 𝐌𝐚𝐫𝐤𝐞𝐭

The IMARC Group report covers a comprehensive analysis of the competitive landscape, including detailed profiles of all major players shaping the global steel market. Top companies drive the industry forward through R&D investment, strategic collaborations with automotive and construction sectors, sustainability initiatives, global expansion, and mergers and acquisitions. The following key companies are profiled in the report:

• ArcelorMittal S.A.

• EVRAZ plc

• Gerdau S.A.

• Hyundai Steel Co. Ltd

• JFE Steel Corporation (JFE Holdings Inc.)

• Jiangsu Shagang Group Co. Ltd

• Nippon Steel Corporation

• Nucor Corporation

• Shougang Group Co. Ltd.

• Tata Steel Ltd. (Tata Group)

• thyssenkrupp AG

• United States Steel Corporation

𝐊𝐞𝐲 𝐓𝐚𝐤𝐞𝐚𝐰𝐚𝐲𝐬 𝐟𝐫𝐨𝐦 𝐭𝐡𝐞 𝐑𝐞𝐩𝐨𝐫𝐭

• The report delivers a comprehensive quantitative analysis of all major steel market segments, covering historical trends from 2020 and market forecasts through 2034, offering stakeholders a complete view of market dynamics over a 14-year horizon.

• The research provides the latest intelligence on the key market drivers, challenges, and emerging opportunities shaping the global steel industry, enabling informed strategic decision-making.

• The study identifies and maps both the leading and fastest-growing regional markets worldwide, enabling stakeholders to pinpoint the most lucrative country-level opportunities within each region.

• Porter’s Five Forces analysis evaluates the impact of new entrants, competitive rivalry, supplier power, buyer power, and substitution threats, providing a clear picture of the competitive intensity and overall attractiveness of the global steel industry.

• The competitive landscape section delivers in-depth profiles of key market participants, offering stakeholders insight into competitors’ strategies, strengths, and current market positioning.

• Asia Pacific holds the dominant regional share of over 62.7% in 2025, underpinned by large-scale infrastructure investment, robust automotive manufacturing, and rapidly expanding renewable energy projects across China, India, Japan, and South Korea.

• The global steel market is projected to grow from USD 1,004.9 Billion in 2025 to USD 1,308.7 Billion by 2034, reflecting a steady CAGR of 2.98%, driven by urbanization, defense spending growth, EV manufacturing expansion, and the global energy transition.

𝐎𝐭𝐡𝐞𝐫 𝐓𝐫𝐞𝐧𝐝𝐢𝐧𝐠 𝐑𝐞𝐩𝐨𝐫𝐭𝐬 𝐁𝐲 𝐈𝐦𝐚𝐫𝐜 𝐆𝐫𝐨𝐮𝐩:

Flat Steel Market Research Report

Weathering Steel Market Research Report

𝐄𝐥𝐞𝐜𝐭𝐫𝐢𝐜𝐚𝐥 𝐒𝐭𝐞𝐞𝐥 𝐌𝐚𝐫𝐤𝐞𝐭: https://www.imarcgroup.com/electrical-steel-market

𝐑𝐮𝐛𝐛𝐞𝐫 𝐆𝐥𝐨𝐯𝐞𝐬 𝐌𝐚𝐫𝐤𝐞𝐭: https://www.imarcgroup.com/rubber-gloves-market

𝐂𝐨𝐨𝐥𝐢𝐧𝐠 𝐅𝐚𝐛𝐫𝐢𝐜𝐬 𝐌𝐚𝐫𝐤𝐞𝐭: https://www.imarcgroup.com/cooling-fabrics-market

𝐀𝐛𝐨𝐮𝐭 𝐔𝐬:

IMARC Group is a global management consulting firm that helps the world’s most ambitious changemakers to create a lasting impact. The company provide a comprehensive suite of market entry and expansion services. IMARC offerings include thorough market assessment, feasibility studies, company incorporation assistance, factory setup support, regulatory approvals and licensing navigation, branding, marketing and sales strategies, competitive landscape and benchmarking analyses, pricing and cost research, and procurement research.

𝐂𝐨𝐧𝐭𝐚𝐜𝐭 𝐔𝐬

IMARC Group

134 N 4th St., Brooklyn, NY 11249, USA

Email: sales@imarcgroup.com

Tel: +1-631-791-1145

Website: www.imarcgroup.com

Elena Anderson

IMARC Services Private Limited

+1 201-971-6302

email us here

Legal Disclaimer:

EIN Presswire provides this news content “as is” without warranty of any kind. We do not accept any responsibility or liability

for the accuracy, content, images, videos, licenses, completeness, legality, or reliability of the information contained in this

article. If you have any complaints or copyright issues related to this article, kindly contact the author above.

![]()

Media gallery